The Bookmaker’s Measure: Kelly, Martingale, and the Price of an Edge

The Bettor With a System

Every casino and every bookmaker has met this person. They have a system. It is called the Martingale. The logic is airtight: bet one unit, lose, bet two, lose, bet four — when you finally win, you recover every loss plus one unit of profit. You cannot lose. Eventually you always win.

The bookmaker is not worried about this person.

Understanding why requires looking at the bookmaker’s side of the ledger — and what you find there is not a gambling operation. It is a derivatives pricing desk.

What the Bookmaker Is Actually Doing

A bookmaker takes bets on both sides of an event. Their goal is not to predict who wins. Their goal is to construct a book where they profit regardless of the outcome.

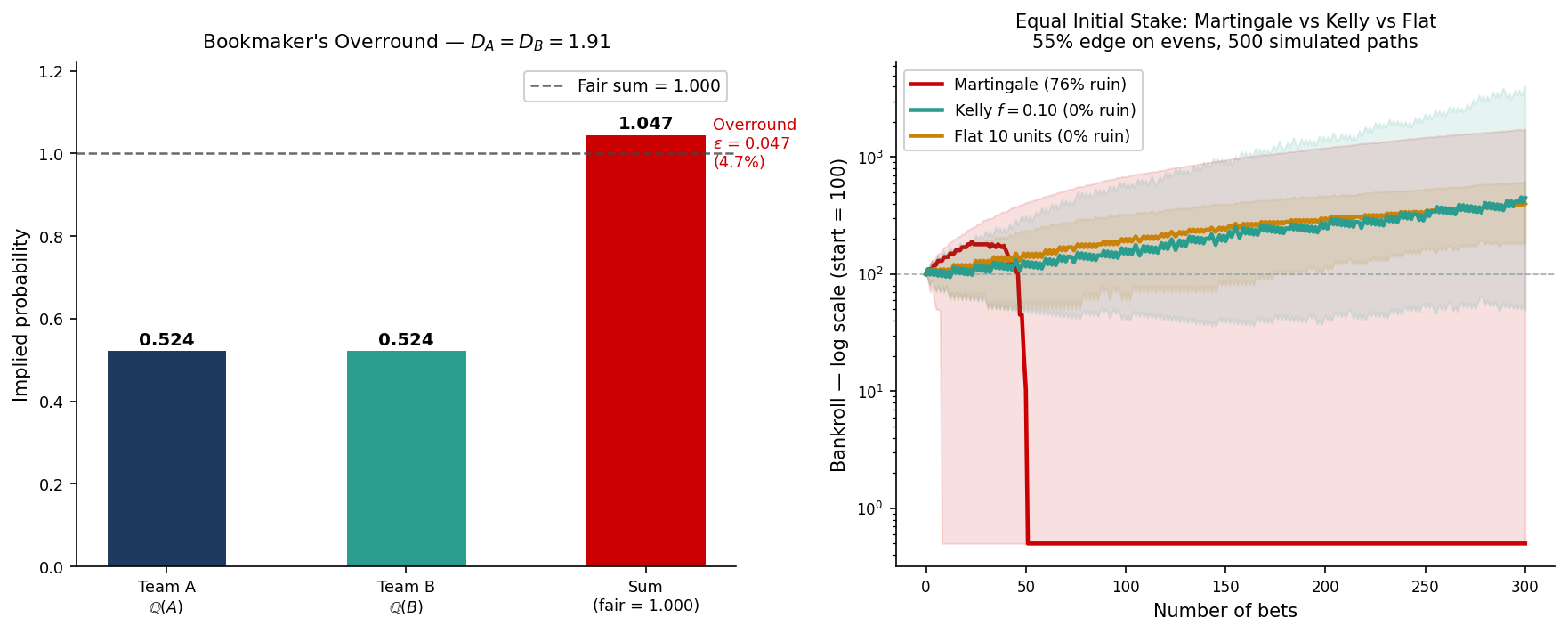

For a match between Team A and Team B, they offer odds $D_A$ and $D_B$. Suppose they take total stakes $S_A$ on Team A and $S_B$ on Team B. Their total intake is $S_A + S_B$. If Team A wins, they pay out $S_A \cdot D_A$. If Team B wins, they pay out $S_B \cdot D_B$.

They want both payouts to be less than the intake. The way they ensure this is by setting odds so that implied probabilities sum to more than one:

$(1)$

The quantity $\varepsilon > 0$ is the **overround** — typically 4–8% in competitive sports markets. Each term $\tfrac{1}{D_i}$ is the market’s implied probability of outcome $i$. If the true probabilities were $p_A$ and $p_B = 1 – p_A$, fair odds would satisfy $\tfrac{1}{D_A} + \tfrac{1}{D_B} = 1$ exactly. The overround is the bookmaker’s margin, baked into the price.

This is not a rule of thumb. It is a precise construction: the bookmaker is defining a **probability measure** $\mathbb{Q}$ under which the expected value of any bet, to the bettor, is negative. Under $\mathbb{Q}$, the bookmaker’s net liability is a martingale — it has no expected change regardless of what happens next. They have engineered a risk-free profit.

Derivatives traders call this the **risk-neutral measure**. The bookmaker is doing exactly what a Black-Scholes desk does when pricing an option: find a measure under which the discounted payoff has zero drift, then charge a premium on top. The overround is the premium.

$(2)$

These normalised implied probabilities define $\mathbb{Q}$. Under this measure, the fair price of any bet is zero. The overround means actual bet prices are always slightly below zero — the bettor pays the spread.

The Bettor’s Problem, Stated Correctly

A bettor with no model is playing under $\mathbb{Q}$. Their expected wealth after $n$ bets:

$(3)$

No betting strategy — Martingale, Fibonacci, flat stake, anything — changes this. The measure is the measure. Changing how much you bet after a loss does not change the expected value of any individual bet. It only changes how the losses are distributed across time.

The Martingale bettor is trying to manufacture edge from the *path* of outcomes. They are solving the wrong problem. Edge does not come from how you sequence your bets. It comes from the gap between $\mathbb{Q}$ and the true probability measure $\mathbb{P}$.

A bettor with a model — one that assigns $\mathbb{P}(A) > \mathbb{Q}(A)$ for some event $A$ — is operating under a different measure than the bookmaker. Their true expected wealth after $n$ correctly-sized bets:

$(4)$

The wealth process has positive drift under $\mathbb{P}$. From the bookmaker’s perspective — who is still pricing under $\mathbb{Q}$ — this bettor looks like any other. The book stays balanced. The bookmaker collects the overround. And yet the bettor compounds steadily, extracting value from the gap between the two measures.

Kelly is the formula that tells you how much to extract.

Kelly as a Measure-Gap Strategy

The Kelly fraction can be written directly in terms of the gap between the true probability and the market’s implied probability. For a binary event with decimal odds $D$:

$(5)$

The exact form depends on the odds structure, but the qualitative message is transparent: $f^* = 0$ when $p^{\mathbb{P}} = \mathbb{Q}(A)$ — no gap, no bet. $f^*$ rises in proportion to the gap. Kelly is not a staking strategy in the conventional sense. It is the optimal exploitation rate for a known mispricing between two probability measures.

This is structurally identical to the position a derivatives trader takes when they believe true volatility differs from implied volatility. They are not guessing which way the stock moves. They are pricing under $\mathbb{P}$ and trading against $\mathbb{Q}$. Delta-hedging extracts the value of the vol mispricing at the optimal rate. Kelly extracts the value of the probability mispricing at the optimal rate.

Why Martingale Fails Even With an Edge

Here is the counterintuitive part. The Martingale strategy fails not only in negative-expected games but in positive-expected ones too.

Suppose our bettor has a genuine edge: $\mathbb{P}(A) = 0.55$ against fair evens ($D = 2.0$, $\mathbb{Q}(A) = 0.50$). The edge is real. Does Martingale work now?

No. The problem is that Martingale is an additive strategy: it responds to recent losses by scaling up bet size absolutely, independent of bankroll. After a losing streak of length $k$, the required stake grows to $s_k = 2^k$ base units. With a starting unit of 10 on a bankroll of 100, the cumulative loss after just four consecutive losses is $\underbrace{10 + 20 + 40 + 80}_{= 150}$ — more than the entire bankroll. A run of four losses wipes you out. That happens with probability $q^4 = 0.45^4 \approx 0.041$, roughly once every 25 sequences. Over 300 bets there are many such opportunities. The simulation confirms it: 76% of paths are ruined within 300 bets despite the 55% edge.

Kelly is multiplicative: it stakes a fixed fraction of the *current* bankroll. After ten losses, the required stake is $f^* \times$ (whatever remains). The fraction is the same. The bankroll shrinks but never hits zero in finite time. Kelly does not respond to recent outcomes at all — only to the current bankroll level and the edge, both of which are known.

Martingale is implicitly claiming: I can generate profit without edge, by being clever about sequencing. Kelly is saying: I have edge, and I will extract it at the mathematically optimal rate, regardless of recent history.

The figure shows what this looks like over 300 bets, with 200 simulated paths per strategy. Each thick line is the median — the middle outcome across all paths. The shaded band runs from the 10th to the 90th percentile: 80% of all paths land inside it.

Kelly’s band is narrow. The 10th and 90th percentile outcomes stay close to the median throughout. Most simulated paths end up near the expected result. The strategy is predictable enough to plan around.

Martingale’s band is wide — and it widens as the simulation progresses. The 90th percentile climbs steeply: paths where the bettor happened to win on large doubled bets compound quickly. The 10th percentile drops toward zero: paths where a long losing streak arrives at the wrong moment, driving the required doubled stake above the remaining bankroll. The Martingale median may track Kelly’s median reasonably closely — both strategies have positive expected value because the edge is genuine. But that median is almost meaningless as a planning number. The spread is so large that “you will probably end up around X” is not a useful sentence for a Martingale bettor. The distribution is not tight enough to plan against.

That is the deeper failure of Martingale. It is not just that it sometimes ruins you. It is that it offers no predictability in return for the risk it takes on. Kelly accepts lower expected wealth than Martingale’s best paths, and in exchange delivers outcomes that cluster tightly around a computable number.

The Unified Picture

The bookmaker constructs $\mathbb{Q}$, extracts the overround, and does not care about outcomes. The Martingale bettor operates entirely within $\mathbb{Q}$ — they have no model, so their expected value is determined solely by the measure the bookmaker set. No strategy survives this.

The Kelly bettor operates under $\mathbb{P} \neq \mathbb{Q}$. They have information the bookmaker does not. Kelly tells them the optimal fraction to stake so that their wealth grows at the maximum rate under $\mathbb{P}$, while remaining — from the bookmaker’s side of the ledger — indistinguishable from any other customer.

Martingale is the wrong answer to the wrong question. The question is not: how do I recover my losses? The question is: what is the gap between my measure and the market’s, and how do I size for it?

Working on a pricing model or risk system? Let’s talk.